The Cannabis Trade/Investment

Why I am going with Green Thumb (GTI) and a smidge of Glass House (GLASF)

Executive Summary

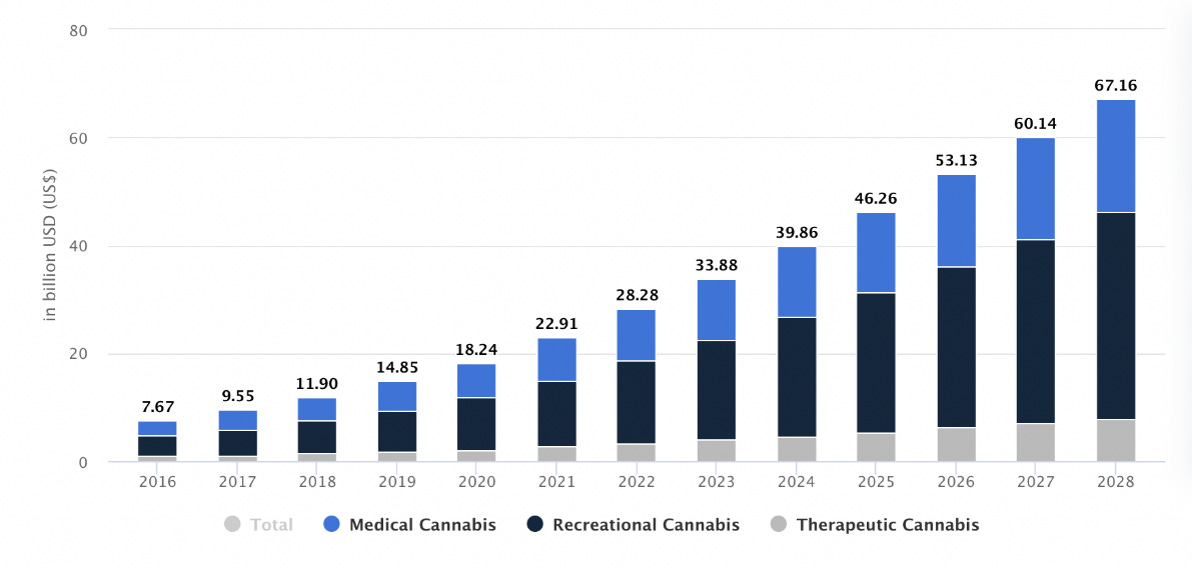

Industry Thesis: The Cannabis thesis centers around a rapid increase in legal demand as the sector moves towards eventual legalization translating into double-digit sales growth through 2030. US cannabis companies look quite inexpensive (single-digit EBITDA multiples) relative to CPG/Alcohol (double-digit EBITDA multiples) and even tobacco companies despite potential growth far in excess of their peers. Today, there is an opportunity to invest in a sector which is under-owned/analyzed, has a clear catalyst with legalization and is likely already a ~$100B industry (only ~$30B legal). The biggest competitor to my two main picks GTI & GLASF is in fact illegal sellers of cannabis which are estimated at around 70% or more of the total market. The below is a good estimate of the market which I believe to be in the right zip code.

This opportunity exists for a variety of reasons mainly structural constraints for institutional investors, stock exchanges, bankers, lenders, marketing, customers etc. due to federal illegality which limits business growth, efficiency, access to capital markets, and most importantly cash flow due to egregious tax laws. Finally, it is impossible to predict how these markets play out over the longer-term which should give all investors pause.

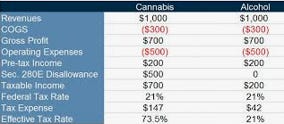

Catalysts: The catalysts to unlock value are plentiful, lead by continued state by state legalization (medical and recreational) and the likely rescheduling of cannabis as a schedule 3 drug (which would allow for a myriad of benefits, the main one is the likely elimination of 280e which taxes companies on gross profits). There are also other legislative movements which could be game-changing such as, allowance of institutional ownership/uplisting, proper banking & advertising, interstate commerce, M&A/consolidation, etc. Arguably, the longer these catalysts take, the wider the moat for strong MSOs (experience, scale, time to build brands, cultivation expertise, retail footprints, customer data etc. before other competition comes in). Below demonstrates the competitive disadvantages currently facing the industry.

Rescheduling: On August 29, 2023, and in response to President Biden’s directive to review cannabis’s scheduling, the Department of Health and Human Services (“HHS”) formally presented its recommendation to the Drug Enforcement Administration (“DEA”) that cannabis be rescheduled to Schedule III from Schedule I. Section 280E does not apply to those trafficking in Schedule III controlled substances. This seems to be for all intents in purposes coming at some point in the near future. There has been multiple hints to this from the President/VP themselves and an easy, popular way to pick up votes. I HATE betting on politicians doing what makes sense, but don't mind as much when its in their own self interest. The Harris/Walz ticket is wonderful for cannabis. Even Donald Trump recently signaled his openness to legalization.

In summary industry revenues could triple without industry growth, strong operators should take more than their share of the growth, huge swaths of new buyers without access will come to the market, legalization will materially increase cash flow, and the companies are not expensive.