Unveiling Portfolio and Track Record

Almost a 15% CAGR Over a Close to 5-year Period

Introduction

Over the past five years, I've been building and iterating an investment style that dances between concentration and diversification. Here is a look at the history of my portfolio since I started tracking my investment performance in earnest almost 5 years ago. I am pleased with the results which have come along with a unique portfolio style. The main thesis is trying to ensure my portfolio is diversified among market factors, but extremely concentrated in nature (8-12 names) so that stock-picking is the main driver of performance.

Performance:

Philosophy:

I have four baskets I place businesses/stocks into: special situations, value, quality, and growth. Within the four, there is really just two. Special situations and value generally go together and act as counterweights to quality and growth. The best combination is getting all four, but that is difficult to find and may come around once every couple of years. This is something like Google in 2011, Meta just last year, or maybe Alibaba today? These situations are never a certainty. In all three situations just listed there was and is very reasonable and compelling counterarguments.

Oftentimes these baskets of stocks move in opposite directions or have large variances in performance depending on the market environment and cycles can be a decade long. One can also define each of these categories in countless different ways. The main idea is simple: I don’t want to be at the behest of market factors and I want my stock selection to determine my performance. See below from JP Morgan for examples of the prior decade’s performances.

In a perfect environment, I allocate my book 50/50 to value/special situations and quality/growth to avoid a factor bet. I bucket loosely and many names will have multiple characteristics or secondary buckets and names can move into and out of each category. The highest I will go as far as the split between value/special situations and quality/growth is 70/30. Again the bottom line is I don’t want to pick factors and I don’t want to underperform for a decade because of the factors I select. I will let the market dictate the attractiveness of the opportunity set and my portfolio exposures will fluctuate within defined parameters based on that opportunity set.

Being dogmatic is okay for some, and the ability of growth and quality investors to explain they are also value investors is not difficult. If your whole portfolio trades for >15x EBITDA or >20x earnings and each company is growing revenues at >10% with a certain ROE you are investing in factors even if you believe that quality/growth name is “cheap”. These names will all move together. To be clear, I think it’s perfectly fine to only pursue one style of investing, but the investor needs to be intellectually honest with oneself and realize that most likely their factor exposure, not their stock-picking is the most important driver of their performance.

This seemingly obvious idea is commonly misunderstood or ignored even at the most sophisticated levels of both portfolio managers and capital allocators. I haven’t done this study, but my guess is substantially all the active fundamental public stock-picking firms that grew over the past decade are quality/growth investors (outside of the pods/quants). If you do the work to compare their performance to the MSCI quality or MSCI Growth indices, many times their alpha goes completely away, however, they have the best returns over trailing 3, 5, and 10-year periods and thus receive the most inflows and the least outflows. Did they become smarter or did their factors work? Did value guys become dumber or did their factors go out of favor?

If the new quality/growth cohort is not able to shift its style, performance will be in line with such factors for the foreseeable future. The next decade, or when factors eventually shift, you’ll see the inevitable rotation and value/special situation firms will come back in style, and quality/growth-only investors will have to start paying attention to value to survive.

Benchmarks

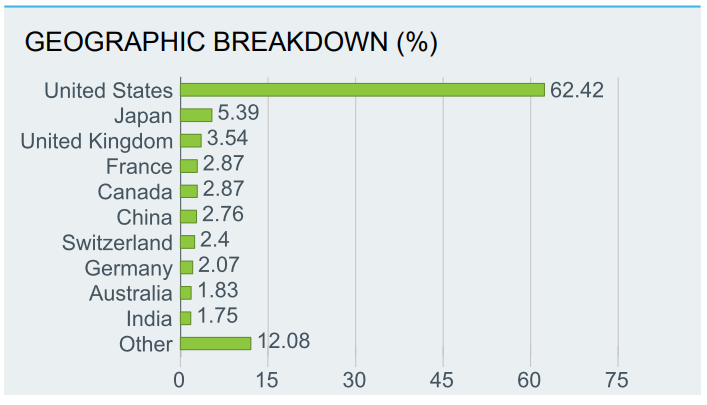

Over the past five years, approximately ~50-70% of my portfolio is US securities while 10-30% has been EM/Frontier with the remainder being ”Ex-US” or developed economies. I don't focus on this in much detail, but I do try to have a global portfolio across the market cap spectrum. For this reason, I generally treat ACWI as my primary benchmark. The ACWI has similar exposures, so my key overweights are really toward small cap and EM. See the ACWI exposures below.

If I were to be more scientific about it, I would utilize a benchmark of 65% Russell 3000, 20% MSCI EM, and 15% ACWI Ex-US. This has performed very similarly to ACWI, so I don’t include it in this article. If I wanted to get extremely scientific I should likely use a global SMID-cap index for ~40-50% or so of my portfolio as my largest overweight vs passive and largely free indices is having a lot of mid-cap and small-cap exposure. This would meaningfully improve my alpha profile. Alternatively, you could argue all strategies should be benchmarked against the SPY. While this does not make much sense to me given the profile of the portfolio, if you were to do so, you’d see my alpha profile decline.

Portfolio Makeup

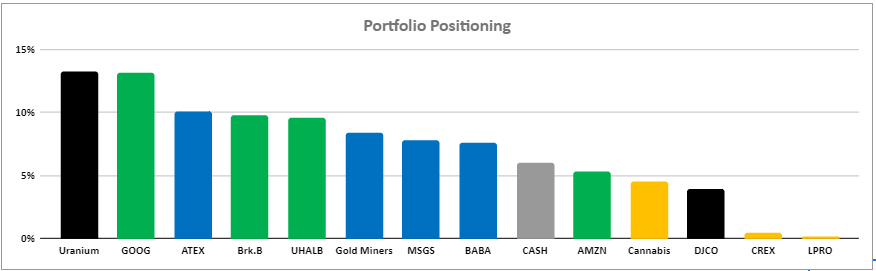

Below is what my current portfolio looks like. While I like my portfolio today, I am in constant search of new opportunities and have a higher cash balance than I would like. Typically when there is a lot of Berkshire and cash in the portfolio it means I don’t have that many bright ideas. Growth and quality opportunities continue to be priced at a premium and my top positions have worse risk/reward from when I first invested (besides ATEX and gold miners).

CREX is a very small position but moved by +50% since my entry. I am unlikely to size up a position if that occurs. I am continuing to do more work on a couple of ideas like LPRO which is a VERY small position, but the market continues to move higher and I am seeing a lack of new ideas at attractive prices.

I’ll discuss position sizing in a separate post.

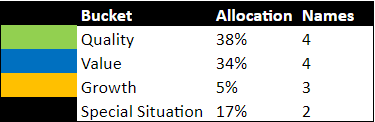

Below is how I “bucket” my current portfolio.

I’ve written a couple of articles thus far in my substack journey on UHAL, ATEX, Uranium, and MSGS all of which were received well. I hope to continue to add to this repository going forward. I may also write up my Cannabis ideas, DJCO, or LPRO in the future.

I am on the search for growth names that have the opportunity to surprise to the upside. I would love to get the growth allocation up to 10-20%. Let me know if you have any bright ideas.

Bright Ideas

Disclaimer: The information provided in this report is for general informational purposes only and should not be construed as investment advice. The author of this article is not a licensed financial advisor and does not guarantee the accuracy, completeness, or timeliness of any information presented herein. Investing in securities or other financial products involves risk, and the reader should carefully consider their own investment objectives, risk tolerance, and financial situation before making any investment decisions. The reader should also consult with a licensed financial advisor or other professional before making any investment decisions. The author of this article will not be held responsible for any losses or damages resulting from any investment decisions made based on the information presented in this article.